Live Backtest Results

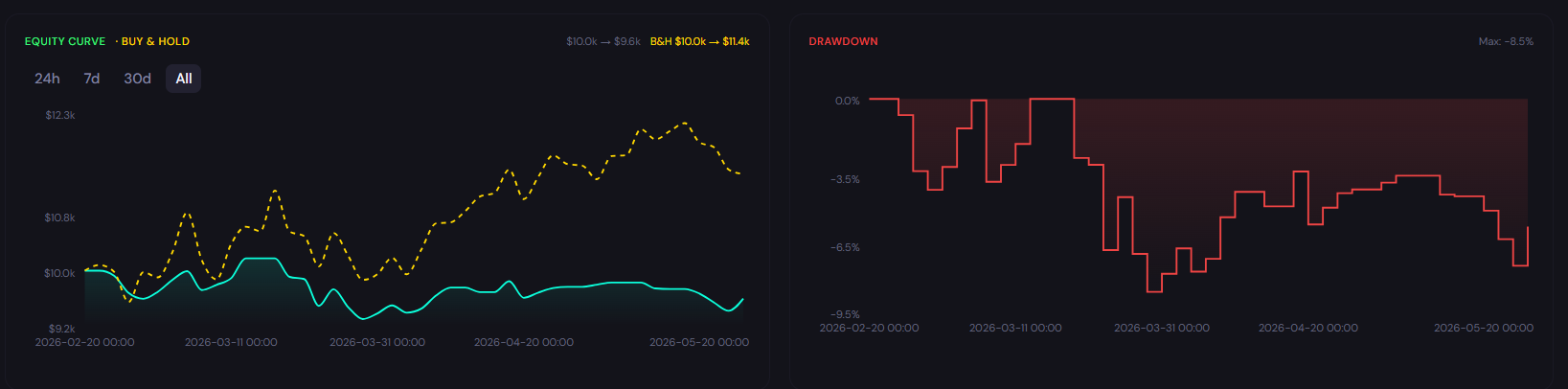

This backtest analyzes the performance of the Bollinger Bands strategy on BTC/USDT over the 45 Minute timeframe using historical market data. The results provide insight into how the strategy would have performed under real market conditions, including profitability, risk exposure, and consistency.

ROI

1.60%

Win Rate

64.3%

Max DD

8.54%

Sharpe

0.44

Profit Factor

1.06

Total Trades

42

Backtest insights

The Bollinger Bands strategy generated a total return of 1.60%, indicating moderate profitability. The maximum drawdown of 8.54% suggests moderate risk exposure. With a win rate of 64.3% across 42 trades, the strategy demonstrates a limited but useful sample size.

Performance may vary depending on market conditions. During trending periods, the strategy may behave differently compared to ranging markets, impacting both returns and drawdowns.

How the Bollinger Bands Strategy Works

What It Is

Bollinger Bands (20,2) are among the most widely used technical indicators in trading. They create a volatility-adjusted envelope around price using a 20-period simple moving average and outer bands 2 standard deviations apart. This particular strategy applies a mean-reversion rule, buying when the market appears oversold at the lower band and selling when price returns toward the average at the middle band.

How Signals Are Generated

In this strategy, a buy signal fires when BTC/USDT closes beneath the lower Bollinger Band (20,2), indicating a short-term oversold condition. The position exits when price crosses back above the 20-period simple moving average. With 45 Minute candles, signals appear frequently: the backtest recorded 42 individual trades. This pace makes the strategy responsive but also sensitive to transaction costs and slippage.

When It Works Best

This strategy tends to perform best during intraday sessions where BTC/USDT oscillates predictably between short-term extremes. On the 45 Minute timeframe, it excels in quiet, low-volatility hours where quick reversions at the bands allow the strategy to compound small gains over many trades.

When It Performs Poorly

However, the strategy may underperform in fast-moving markets where execution quality deteriorates. On the 45 Minute timeframe, even a modest drop in fill quality across many trades can turn a positive backtest into a losing live outcome. Slippage during volatile periods is the primary risk factor.

Strengths

Fast signal generation means the strategy adapts quickly to changing intraday conditions

Systematic rules remove hesitation and emotion from high-speed decision-making

Small, repeated gains compound effectively when the win rate is favorable

Limitations

Transaction costs and slippage have a proportionally larger impact due to high trade frequency

Random intraday noise generates false signals that the strategy cannot reliably distinguish from genuine reversals

As a lagging indicator, RSI and BB signals on fast timeframes can enter after the move has already started

Why Use CoinQuant Instead of Manual Trading or Other Platforms

Choosing the right way to test and execute trading strategies is critical. Below is a comparison between CoinQuant, manual trading, and other platforms to highlight key differences in speed, accuracy, and usability.

CoinQuant is designed specifically for traders who want to validate strategies quickly and reliably without coding. Unlike manual trading or traditional platforms, it allows you to test multiple scenarios, analyze performance instantly, and iterate faster using real data.

Frequently asked questions

How does the Bollinger Bands strategy perform on BTC/USDT in the 45 Minute timeframe?

The performance of the Bollinger Bands strategy on BTC/USDT in the 45 Minute timeframe depends on market conditions. Based on the backtest results above, it achieved a return of 1.60% with a maximum drawdown of 8.54%. Results may vary depending on volatility and overall market trends.

Is the Bollinger Bands strategy reliable for trading BTC/USDT?

The Bollinger Bands strategy can be effective when used in the right conditions. For BTC/USDT, it typically performs well in range-bound intraday conditions with regular price oscillations between well-defined short-term extremes but may underperform during fast-moving news-driven markets, extreme volatility events, and conditions where spreads widen significantly. Backtesting helps evaluate its reliability before applying it in live trading.

Why is backtesting important for trading strategies?

Backtesting allows traders to evaluate how a strategy would have performed using historical data. It helps identify strengths, weaknesses, and risk levels before applying the strategy in real markets, reducing the likelihood of unexpected losses.

How can I test the Bollinger Bands strategy on CoinQuant?

You can use CoinQuant to build and backtest the Bollinger Bands strategy without coding. Simply type the prompt shown below into the CoinQuant chat box and the platform will parse your natural language instruction, generate the strategy logic, and run the full backtest automatically.

What are the best settings for the Bollinger Bands strategy on the 45 Minute timeframe?

The best settings for the Bollinger Bands strategy depend on the asset and timeframe. On shorter timeframes, traders sometimes widen to 2.5 standard deviations to reduce noise or tighten to 1.5 for faster signals. The period can also be shortened (from 20 to 10 or 14) to generate more frequent entries, though this increases sensitivity to false signals. Using a backtesting platform like CoinQuant allows you to test different configurations and identify what works best.