CoinQuant vs Gainium: Which One Has Better Backtesting?

Gainium and CoinQuant both offer crypto trading tools, but they serve different missions. Gainium is an automation platform: it excels at executing strategies across exchanges with bots and smart orders. CoinQuant, the no-code AI trading platform, is a research and validation platform: it gives you tick-level backtesting, strategy analytics, and data from Kaiko across Binance, Coinbase, and Kraken. If you want to automate a strategy you already trust, Gainium is solid. If you want to find, test, and validate whether a strategy actually works before automating it, CoinQuant is built for that. Here is the breakdown.

Head-to-Head Comparison

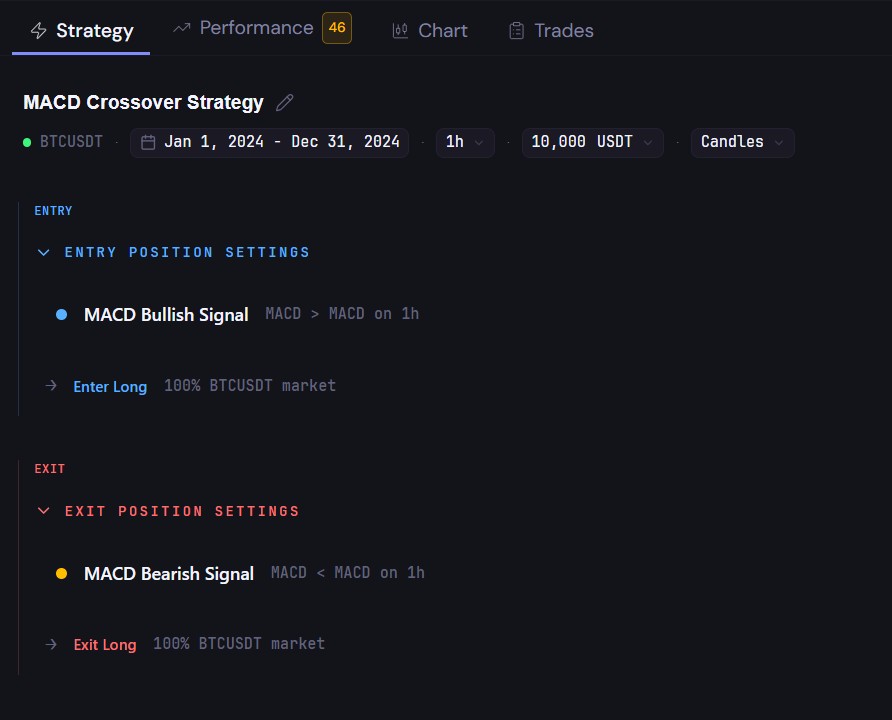

Real Example: MACD Crossover on BTC

To make this concrete, we ran the same MACD(12/26/9) crossover strategy on BTC/USDT 1h for all of 2024 on CoinQuant. Starting with $10,000:

Total Return: +16.5% ($10,000 to $11,647)

Sharpe Ratio: 0.59 (modest risk-adjusted return)

Win Rate: 36.7% (low, but wins are 1.8x bigger than losses)

Max Drawdown: 22.9% (sizable peak-to-trough decline)

Total Trades: 332 (statistically robust sample)

Profit Factor: 1.06 (barely profitable after fees)

The MACD crossover is not a great strategy on its own - the 0.59 Sharpe and 22.9% drawdown tell you that immediately. But that is exactly the point: CoinQuant surfaces these weaknesses in seconds so you can refine or discard the strategy. Gainium would execute this same strategy efficiently across exchanges, but it would not tell you the strategy has a 36.7% win rate before you start trading it.

The Ideal Workflow: Both

These platforms complement each other. Validate on CoinQuant first: run backtests, check the 5-point framework, refine your strategy until the Sharpe, drawdown, and profit factor clear the bar. Automate on Gainium after: once you have a validated strategy, deploy it with Gainium’s bot automation across your exchanges. The traders who do both outperform the traders who do one or neither.

Validate your strategy on CoinQuant before you automate it - start free.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.