What Is Crypto Day Trading? And How Do You Backtest a Day Trading Strategy?

.png)

Most crypto day trading content tells you what it is and stops there. The more important question gets skipped: how do you know if your day trading strategy actually works before you put real capital behind it?

This article defines what is crypto day trading, explains what a day trading strategy needs to be viable, and walks through how to backtest a day trading strategy on CoinQuant so you can test your ideas with historical data before taking any live trades.

What Is Crypto Day Trading?

Crypto day trading means opening and closing positions within the same trading day. In practice, this often means holding a trade for minutes to a few hours rather than overnight. The defining rule: no positions are held when you step away from the market for the session. Every trade opens and closes within a defined window.

On traditional stock markets, "the day" is defined by exchange hours (9:30 AM to 4:00 PM in the US). Crypto has no such boundary. Markets run 24 hours a day, seven days a week. In crypto, day trading is more accurately described as short-duration trading: positions held for minutes to several hours, not days or weeks.

Why Crypto Suits Day Trading

Three structural features make crypto attractive for short-duration strategies:

24/7 markets. Crypto never closes. A day trader can be active at any hour without waiting for a market open. There is no overnight gap risk from markets moving while you are asleep, which is a real risk in equities.

High volatility. Bitcoin regularly moves 3 to 8 percent in a single day. Altcoins can move 10 to 30 percent in hours during active markets. Higher volatility means more short-term price movement, which is the raw material day traders work with.

No shorting restrictions. On many traditional equity markets, short selling has restrictions. In crypto, shorting via perpetual futures is broadly accessible across major exchanges, giving day traders the ability to profit in both directions.

The Reality Check

Day trading crypto is hard. Most retail traders who attempt it without a systematic, tested strategy lose money. The reasons are consistent: trading on intuition without a defined edge, no tested entry and exit rules, improper risk management, and overtrading.

A day trading strategy that has not been backtested is a hypothesis. You are assuming it works based on intuition, not evidence. Backtesting converts that hypothesis into data. It shows you how the strategy would have performed over thousands of historical bars, revealing win rate, how often it loses, how large the losses are, and whether there is any actual edge in the rules.

Without that data, you are trading opinion. With it, you are trading evidence.

What a Day Trading Strategy Actually Needs

A valid day trading strategy has four components:

Entry rule. A specific, objective condition that defines when to open a position. Not "buy when it looks oversold." Something like: "Enter long when RSI(14) crosses above 30 from below on the 15-minute chart."

Exit rule. A specific condition that defines when to close the position. This can be a profit target, an indicator signal, or a time-based exit such as closing all positions after four hours.

Risk per trade. The maximum amount you are willing to lose on any single trade, usually expressed as a percentage of capital. Without this, a series of losses compounds quickly.

Timeframe. Day trading uses short timeframes: 1-minute, 5-minute, 15-minute, or 1-hour charts. The timeframe affects how many signals you get and the size of typical price moves.

The more specific these four components are, the more reliably you can backtest the strategy and the more consistently you can execute it.

Why Backtesting Matters Especially for Day Traders

Higher trading frequency is actually an advantage when backtesting. A swing trader who holds positions for days or weeks might complete 50 trades over a year. That is barely enough data to draw conclusions. A day trader on the 1-hour chart might complete 200 to 500 trades over the same period.

More trades mean more data points. More data points mean you can measure your strategy's actual win rate, typical profit factor, and real drawdown behavior with statistical confidence. The feedback loop is faster: you learn more, faster, from a day trading backtest than from a longer-term strategy.

For day traders specifically, backtesting is not optional. It is how you build the evidence base that tells you whether your strategy has an edge.

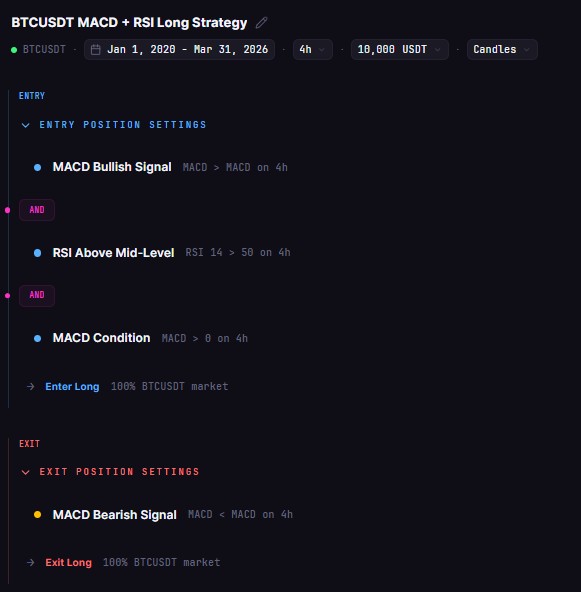

How to Backtest a Day Trading Strategy on CoinQuant

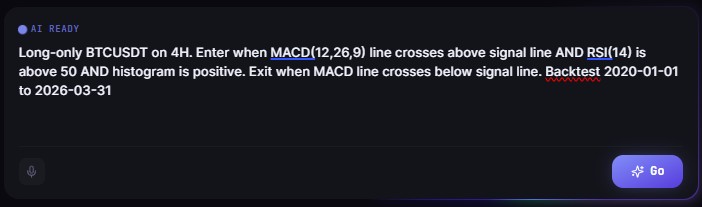

CoinQuant's strategy builder accepts natural language descriptions. You describe your day trading strategy in plain English and the AI builds the backtest conditions automatically. No Pine Script, no Python required.

Here is a simple step-by-step for a basic RSI day trading strategy:

Open the strategy builder on CoinQuant

Select your asset: BTC/USDT (or any crypto pair)

Set the timeframe to 1H or 15m

Describe your strategy: "Enter long when RSI(14) crosses above 30 from below. Exit when RSI(14) crosses above 70 or after 8 candles."

Set fees: 0.1% per trade

Set initial capital: $10,000

Run the backtest

The platform returns a full results dashboard with every metric you need to evaluate the strategy.

Key Metrics to Check in Your Day Trading Backtest

Not all metrics matter equally for day trading. These are the ones to focus on:

Win rate. What percentage of trades were profitable? A day trading strategy with a 40% win rate can still be profitable if winning trades are larger than losing ones. Win rate alone does not tell you whether a strategy works.

Profit factor. Gross profit divided by gross loss. A profit factor above 1.5 suggests a real edge. Below 1.0 means the strategy lost money overall. This is the single most important number for evaluating whether a strategy has an edge.

Maximum drawdown. The largest peak-to-trough decline in your account balance during the backtest period. For day traders, keeping this below 20% is a reasonable baseline. Large drawdowns require large recoveries: a 50% drawdown requires a 100% return just to get back to even.

Average trade duration. For a day trading strategy, check that trades are actually closing within your intended window. If the average trade is held for 3 days when you expected hours, the exit logic needs adjustment.

What to Do After Your Backtest

A backtest result is the beginning of the process, not the end. If the results look strong, the next steps are:

Check for overfitting. A strategy tuned specifically to one period of market data may not perform well in other periods. Test the same strategy on different date ranges and different assets to see if the edge holds.

Paper trade it. Before committing real capital, forward-test the strategy in real market conditions using paper trading. This validates that the strategy behaves as expected in live price action, not just historical data.

Start small. The first live trades with any strategy should be small size. You are testing real execution conditions, not just strategy logic.

For a specific example with RSI on Bitcoin's 1-hour chart and 3 years of backtest data, see our Day Trading Bitcoin with RSI article

Start Backtesting Your Day Trading Strategy

CoinQuant is designed for this exact workflow. Describe your day trading strategy, run a full backtest on real Kaiko data, and get the metrics you need to decide whether the strategy is worth trading live.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.

Key Takeaway