Trading Simulator vs Backtesting vs Paper Trading: Which One Actually Predicts Real Results?

.png)

The trading simulator vs backtesting debate confuses a lot of traders, because all three tools, simulators, backtests, and paper trading, promise the same thing: proof that a strategy works before you risk money. They do not measure the same thing, and only one of them tests your actual rules against history.

This article defines all three clearly, then answers the real question with data: does a strong backtest actually predict forward results? We ran the same Bitcoin strategy across two separate time periods to find out, and the gap between them is the whole lesson.

Trading Simulator vs Backtesting vs Paper Trading, Defined

They sound interchangeable. They are not.

Backtesting runs a fixed set of rules against real historical price data and reports exactly how the strategy would have performed. It is fast, repeatable, and objective. You get metrics like return, win rate, Sharpe ratio, and drawdown on data that already happened.

A trading simulator lets you place trades against historical or replayed market data to practice execution and get a feel for how a market moves. The focus is on the human learning to trade, not on validating a fixed rule set.

Paper trading runs a strategy forward against live market prices without real money. It tests how rules behave on data that has not happened yet, in real time, which is slower but closer to live conditions.

The Question That Actually Matters

Definitions are easy. The hard question is the one traders care about: if a strategy backtests well, will it keep working?

This is where backtesting earns both its value and its bad reputation. A backtest tells you what happened. It cannot promise the future looks like the past. The only honest way to see the gap is to test a strategy on one period, then check it on a completely separate one it never saw.

That is exactly what we did.

The Test: Same Strategy, Two Separate Periods

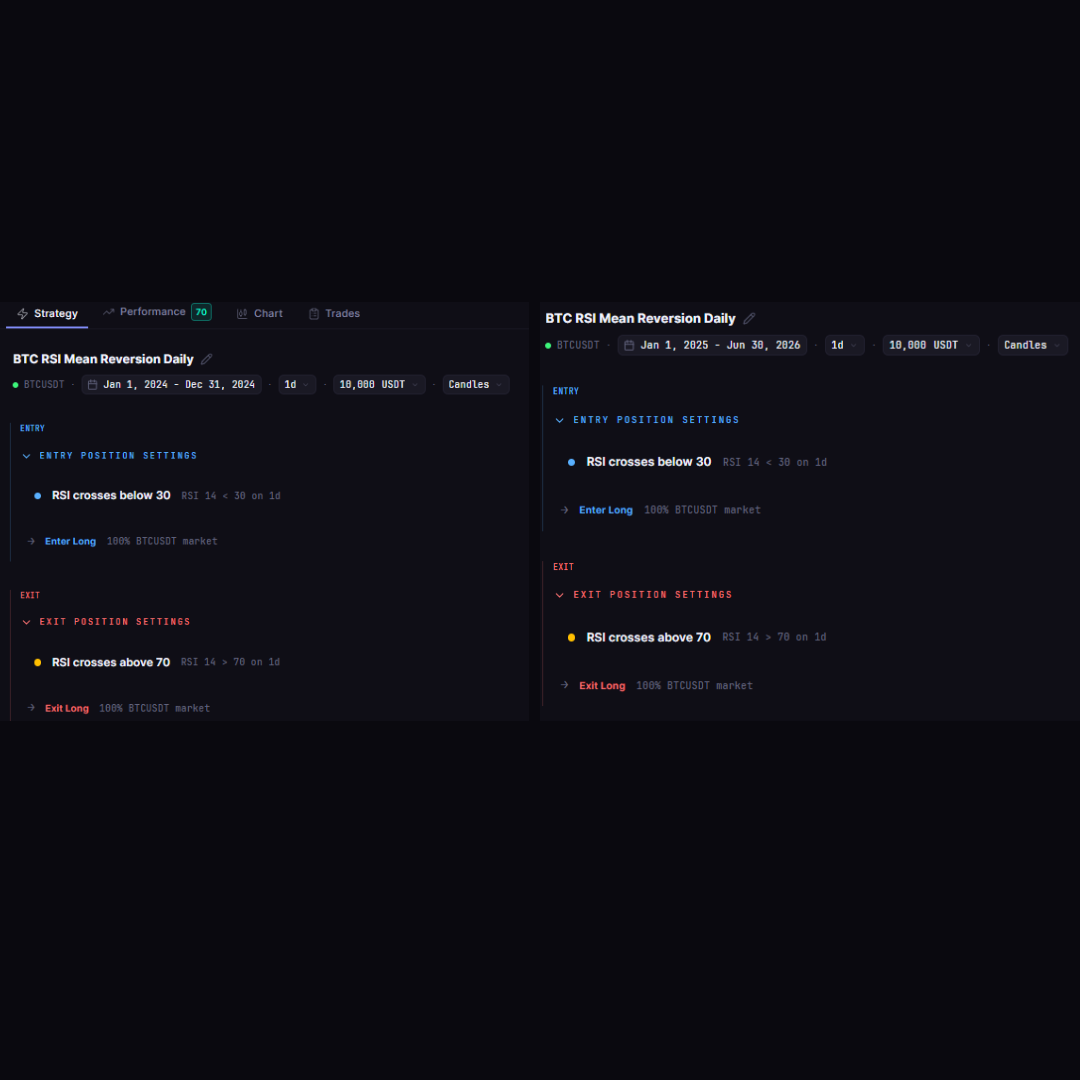

We used a simple, well-known rule so the result is about method, not magic: RSI(14) mean reversion on Bitcoin. Enter long when RSI crosses below 30, exit when it crosses above 70. Daily candles, no leverage, one position at a time.

Then we ran it on two non-overlapping windows:

In-sample: 2024, the period you might have "discovered" the strategy on

Out-of-sample: 2025 to June 2026, the forward period it never touched

Data sourced through Kaiko via CoinQuant. Fees included. Initial capital $10,000.

.png)

.png)

What the Data Actually Shows

On the 2024 data, the strategy looked good. A +14.45% return with a 100% win rate is the kind of result that makes a trader confident enough to risk real money.

Then the same rules, unchanged, ran forward into 2025 and 2026 and lost 14.56%. The win rate dropped, the Sharpe ratio went negative, and the profit factor fell to 0.50, meaning it made 50 cents for every dollar it lost.

Nothing about the strategy changed. Only the market did. A backtest that looked like a winner on one period was a loser on the next.

There is an honest caveat: the 2024 window produced only one trade, which is far too small a sample to trust on its own. That is itself part of the lesson. A single lucky trade can make a backtest look flawless, and mistaking that for a validated edge is how traders get hurt.

Why This Gap Exists

A backtest is a measurement of the past, and markets change regime. A strategy tuned to one environment, a calm uptrend, a specific volatility level, often fails when the environment shifts.

This is where the three tools connect:

Backtesting on a single period can flatter a strategy that got lucky

Backtesting across multiple periods and regimes exposes whether the edge is real or a fluke

Forward methods like paper trading add a final check on data the strategy has never seen

The failure above was not a failure of backtesting. It was a failure of testing on too little. The fix is not to abandon backtests. It is to backtest harder: across bull legs, bear legs, and separate in-sample and out-of-sample windows.

How to Use Backtesting So It Actually Predicts

A backtest predicts forward results only when you use it honestly. The practices that matter:

Test across multiple regimes, not one comfortable stretch. Include a downtrend.

Split your data. Validate on a period the strategy was never shaped on.

Judge by profit factor and drawdown, not win rate. A 100% win rate on one trade proves nothing.

Demand a real sample. A handful of trades is a hint, not a verdict.

Include fees. An idealized backtest overstates every result.

A strategy that survives all of that is far likelier to hold up forward than one that looked perfect on a single lucky year.

The Bottom Line

Simulators teach you to trade. Paper trading checks a strategy forward in real time. Backtesting is the fastest, most objective way to find out whether a rule set ever had an edge, and it is the foundation the other two build on.

The catch is that a backtest is only as trustworthy as the data you run it across. Test one period and you get a story. Test many, split your samples, and read the right metrics, and you get something close to a prediction.

Backtest Before You Simulate, Start Free on CoinQuant

You do not need to code. Describe a strategy in plain English, run it across multiple periods of real Bitcoin data with fees included, and see for yourself whether the edge holds out of sample before you risk a dollar.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.

Key Takeaway