Is No-Code Backtesting Suitable for All Trading Strategies?

.png)

No-code backtesting has made strategy validation accessible to traders who do not know Python or Pine Script. The honest question is whether no-code backtesting is suitable for all trading strategies, or whether certain approaches require code-based tools to test accurately. The answer is: no-code is appropriate for the vast majority of strategies that retail and semi-professional traders actually want to test. But there are real limits, and knowing them helps you understand what you can and cannot conclude from a no-code backtest.

What No-Code Backtesting Actually Does

In a no-code backtesting platform like CoinQuant, the input is a strategy description in natural language. The AI interprets the logic, builds the strategy conditions programmatically, and runs the simulation against historical price data. The trader never writes a line of code.

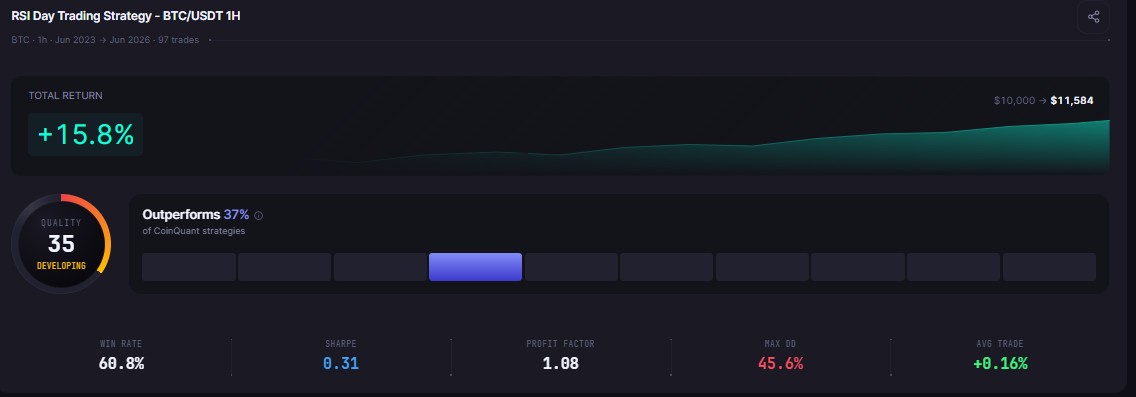

This means the no-code approach works for any strategy that can be expressed clearly in natural language: "Buy BTCUSDT when RSI(14) crosses above 30 on the daily chart, with the 21-day EMA above the 55-day EMA. Sell when RSI crosses above 65." That is a complete, testable strategy. No coding, no configuration. The AI can parse it and run it.

The no-code constraint is not really about complexity of the strategy logic. CoinQuant supports multi-indicator conditions, multi-timeframe filters, multi-asset strategies, and configurable position sizing. The constraint is about specificity of the description. A strategy that can be described precisely in natural language can be tested no-code. A strategy that requires custom mathematical transformations, dynamic position sizing based on portfolio volatility, or execution logic that depends on order book data generally cannot.

Strategies That Work Well in No-Code Backtesting

The following strategy types are well-suited to no-code backtesting and can be fully tested using CoinQuant's AI strategy builder:

Indicator-based entry and exit strategies: Any strategy using standard indicators, including RSI, EMA, MACD, Bollinger Bands, ATR, and Volume conditions, can be described in natural language and tested accurately. This covers the majority of strategies that retail traders want to validate.

Mean reversion strategies: "Buy when RSI drops below 30 and recovers" is a simple description of a complete, backtestable mean reversion setup. The AI correctly handles the two-condition logic (below threshold, then recovery) without requiring code.

Trend-following strategies: "Buy when the 21-day EMA crosses above the 55-day EMA; sell when it crosses below" is a textbook trend-following approach. No-code handles this cleanly.

Multi-condition strategies: Combining multiple indicators in an entry condition is supported via natural language. "Buy when RSI is below 40 and price closes above the 20-day EMA and daily volume is above the 20-day average volume" is a three-condition entry. CoinQuant's AI can parse and test this.

Multi-timeframe confirmation: CoinQuant supports multi-timeframe strategies, where you might require a signal on the daily chart with a confirmation on the four-hour chart. This can be described naturally and tested accurately.

Strategies That Require Code-Based Tools

There are strategy types where code-based platforms provide capabilities that no-code tools currently do not. Being clear about these limits prevents overconfidence in results from strategy types that fall outside the no-code scope:

High-frequency and sub-minute strategies: Scalping strategies that depend on tick data or sub-minute candles with precise order timing typically require code to handle execution simulation accurately. No-code platforms operate on candle data (one minute and above), not tick data.

Portfolio-level optimization: Strategies that dynamically allocate capital across many assets simultaneously based on cross-asset correlations or portfolio-level volatility targets require code to implement correctly. These are primarily institutional portfolio management strategies rather than single-asset trading strategies.

Custom mathematical transformations: If your strategy requires a proprietary indicator that does not exist in a standard library (for example, a custom oscillator derived from your own mathematical formula), you will need to implement it in code. No-code platforms work with established indicator libraries.

Order-book-dependent strategies: Market-making strategies, strategies based on bid-ask spread dynamics, or approaches that depend on order flow data cannot be backtested meaningfully on candle-based historical data, regardless of whether the platform is code-based or no-code.

A Plain-English Example of What Works

Here is a moderately complex strategy that a trader might want to test, described exactly as you would type it into CoinQuant:

"Buy BTCUSDT on the daily chart when RSI(14) closes below 35 and EMA(21) is above EMA(55) and today's volume is above the 20-day average volume. Sell when RSI crosses above 65 or when EMA(21) crosses below EMA(55). Test using Kaiko data from 2019 to 2024."

This is a three-condition entry with a dual-condition exit. It combines mean reversion (RSI oversold), trend context (EMA relationship), and volume confirmation. All three conditions are standard indicators. The strategy can be described clearly and precisely in natural language.

CoinQuant will interpret this, build the condition logic, run the backtest on Kaiko institutional data, and return the full metric set in seconds: Sharpe Ratio, Profit Factor, Max Drawdown, CAGR, and the Strategy Quality Score.

What No-Code Backtesting Changes for Retail Traders

Two years ago, running an institutional-quality backtest with a Sharpe Ratio and full risk metric set required coding ability or a developer. That analysis was not accessible to most retail traders.

No-code backtesting changes this. The technical barrier to a comprehensive backtest on institutional-grade data is now close to zero. The barrier is now strategy thinking: traders who understand what indicators measure and how to construct a logical entry and exit condition get more from these tools than those who treat the platform as a black box.

If you have a trading idea and have not tested it on historical data, there is no longer a good reason not to.

Common Mistakes When Using No-Code Backtesting

Assuming the strategy is validated after one backtest. A single backtest on one asset and one period is a starting point, not a conclusion. Run the same strategy across multiple assets and historical windows before forming a view.

Relying on strategies that cannot be clearly described. If you cannot write down the entry and exit conditions precisely in plain language, the strategy is not defined clearly enough to backtest accurately, whether in code or no-code. Precision in strategy description is a prerequisite for reliable backtesting in any format.

Treating no-code as less rigorous than code. Output quality depends on data quality, simulation accuracy, and metric depth. CoinQuant uses Kaiko institutional data, models fees at 0.1% per trade, and returns 17 metrics. The no-code input does not reduce the rigor of the output.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.

Key Takeaway