Does Buying the Dip Work in Crypto? 9 Years of Backtested Evidence

"Buy the dip" is the most repeated advice in crypto. Price drops, someone says it, and it sounds obviously correct. Buy low, wait for the recovery, profit. So does it actually work?

We ran a mechanical buy-the-dip strategy on Bitcoin across six years of data to find out. The result answers does buying the dip work with real numbers, and the honest answer is more nuanced than the slogan: it was right most of the time and still lost money.

What "Buying the Dip" Really Means

As a slogan it means nothing precise. As a strategy it has to be defined: what counts as a dip, and when do you sell?

The version tested here uses a clear, common definition:

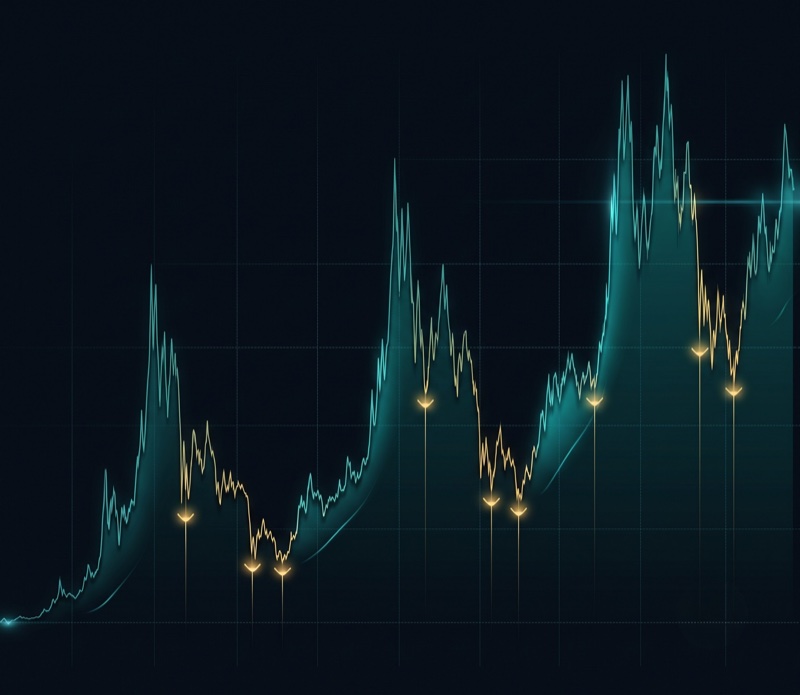

A dip is when price falls sharply below its recent average, specifically below the lower Bollinger Band.

You sell when price recovers back to the average, the middle Bollinger Band.

This is textbook dip-buying: buy the sharp drop, sell the reversion to the mean. Mechanical, repeatable, and testable.

The Strategy We Tested

A single buy-the-dip rule on spot Bitcoin.

Entry (long):

Close crosses below the lower Bollinger Band (20-day, 2 standard deviations). Price has dipped hard.

Exit:

Close crosses back above the middle Bollinger Band (the 20-day average). The dip has recovered to the mean.

You can build this on CoinQuant in plain English. No Python. No Pine Script.

Backtest Setup

Every number below comes from a single backtest on CoinQuant. Nothing is estimated.

Instrument: BTCUSDT, spot

Timeframe: Daily

Period: January 1, 2020 to June 30, 2026

Data: Kaiko via CoinQuant (Binance, Coinbase, Kraken)

Fees: 0.1% per trade

Leverage: None

Initial capital: $10,000

Six years covers two bull runs and two brutal drawdowns, giving the strategy dozens of real dips to buy.

The Results

The strategy bought 38 dips, won most of those trades, and still finished down, while simply holding Bitcoin returned many times more.

Why Being Right 63% of the Time Still Lost

The strategy won nearly two out of every three trades. It still lost 13%. Two structural problems explain the gap.

First, the winners were small. Selling at the mean caps each trade at the bounce back to average, so profitable dips paid modestly.

Second, the losers were large. When a dip kept dipping, as it did through the 2022 bear, price fell far below the lower band and stayed there. Those trades gave back much more than the small winners earned. A high win rate hid a lopsided payoff.

The Bigger Cost: The Trend You Missed

The most important number is the comparison. Holding Bitcoin from 2020 to 2026 returned +714.1%. The dip-buying strategy lost 13%.

By selling every recovery at the mean, the strategy exited right before the largest sustained rallies. Buy-the-dip is a mean-reversion strategy, so it is built to capture small reversions and structurally miss the big trends that produced almost all of Bitcoin's return.

The one real benefit was a smaller drawdown, 52.2% versus 76.6% for buy-and-hold. Less pain, but also nowhere to go.

So, Does Buying the Dip Work?

As tested, no. Not as a standalone mean-reversion rule on Bitcoin over this period. It was frequently right and still unprofitable, and it badly trailed doing nothing.

That does not mean the idea is worthless. It means the naive version is. Things worth testing next:

Let winners run. Replace the mean-reversion exit with a trailing stop so recoveries that turn into trends are not cut short.

Filter the dips. Only buy dips when a longer-term trend is up, to avoid catching every knife in a bear market.

Size for the losers. Smaller positions on the deepest dips can shrink the trades that did the damage.

Each is a separate backtest. That is how a slogan becomes a strategy, or gets retired.

The Takeaway

Buying the dip felt right, tested wrong. On Bitcoin from 2020 to 2026 it won 63% of its trades, lost 13% overall, and missed a 714% trend. Before you buy the next dip, test your exact rules. The data will tell you whether you are buying value or averaging into a downtrend.

The Difference Between a Dip and a Downtrend

The slogan buy the dip quietly assumes you can tell a dip from a downtrend in advance. You cannot, at least not reliably. A dip is a temporary fall inside an uptrend. A downtrend is a series of dips that keep going. They look identical at the moment you are deciding to buy.

Our backtest bought 38 dips and won 63% of them, yet still lost 13%. The winning trades were the real dips inside uptrends. The losing trades were the dips that turned out to be a downtrend, and those losers were large enough to erase all the small wins and then some.

Why the Mean-Reversion Exit Capped the Upside

The strategy sold when price recovered to its average. That is a sensible mean-reversion exit, and it is also why the strategy could never capture a real trend. Every time a dip turned into a sustained rally, the strategy sold early, at the mean, and watched the rest of the move happen without it.

Over 2020 to 2026, holding Bitcoin returned +714%. Almost all of that came from sustained trends, precisely the moves a mean-reversion exit is designed to leave on the table. The strategy was structurally built to miss the thing that mattered most.

Turning the Slogan Into a Strategy

Add a trend filter so you only buy dips when the longer-term trend is up, avoiding the downtrend dips that did the damage.

Replace the mean-reversion exit with a trailing stop, so recoveries that become trends are allowed to run.

Manage the losers, through position sizing or a stop, since a few large losses defined this result.

Each idea is testable. That is the point of backtesting: it turns a comforting phrase into a set of rules you can measure, keep, or discard on evidence.

Frequently Asked Questions

So buying the dip never works?

As a naive standalone rule over this period, it lost. That does not mean the idea is worthless, it means the simple version is. Filtered and combined with better exits, dip-buying can be worth testing.

Why did it lose with a 63% win rate?

Small winners, large losers. Selling at the mean capped the wins, while dips that became downtrends produced the big losses.

The Psychology the Numbers Expose

Buying the dip is as much an emotional strategy as a technical one. It feels smart, decisive, and contrarian, and that feeling is exactly what the backtest strips away. Winning 63% of trades kept the feeling alive while the account quietly bled, because the memorable wins hid the larger losses.

This is the value of testing a slogan. The market rewards processes, not feelings, and a backtest is the cleanest way to find out whether your process matches your intuition. Here it did not. The dip-buyer felt right on most trades and still finished behind someone who did nothing but hold. That gap between feeling right and being profitable is where most trading accounts are lost.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.

Key Takeaway