Bitcoin Bottom-Fishing Strategies Backtested: What Actually Worked in Past 50% Drawdowns

When Bitcoin is down 50% or more, the same idea grips every trader: this has to be close to the bottom. So they buy the capitulation low, expecting the bounce. It feels smart. It even wins often.

We ran a Bitcoin bottom-fishing strategy backtest on real data to see whether it actually pays. The answer is a useful surprise: the strategy won most of its trades and still lost money, badly trailing a trader who did nothing but hold.

Here is exactly what happened, and why a 60% win rate was not enough.

What Bottom-Fishing Tries to Do

Bottom-fishing means buying an asset after a steep fall, betting the low is in and a recovery follows. In crypto, traders usually anchor it to a deep oversold reading, the point where selling looks exhausted.

The appeal is obvious. You buy low, you sell into the bounce, you repeat. The risk is equally obvious: a level that looks like the bottom can be the middle of a much larger fall.

A rules-based backtest settles the argument by removing the emotion and just counting the outcomes.

The Strategy We Tested

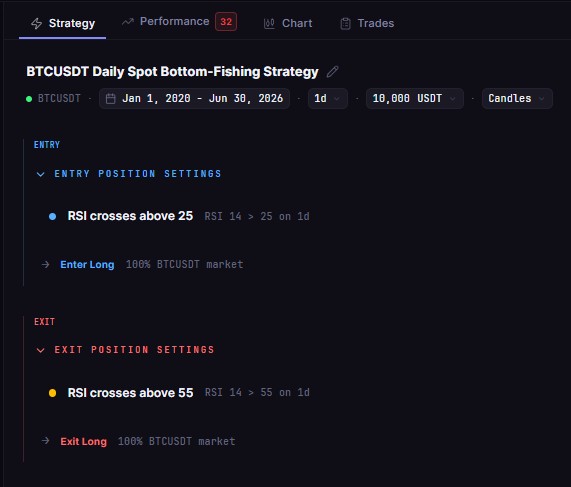

A single, mechanical bottom-fishing rule on spot Bitcoin.

Entry (long):

RSI(14) crosses above 25, recovering from a deep oversold capitulation reading.

Exit:

RSI(14) crosses above 55, taking the bounce rather than waiting for a full trend.

This is the practical version of bottom-fishing: wait for the deepest oversold flush to start recovering, buy the turn, and sell into strength. You can build it on CoinQuant in plain English. No Python. No Pine Script.

Backtest Setup

Every number below comes from one backtest on CoinQuant. Nothing is estimated.

Instrument: BTCUSDT, spot

Timeframe: Daily

Period: January 1, 2020 to June 30, 2026

Data: Kaiko via CoinQuant (Binance, Coinbase, Kraken)

Fees: 0.1% per trade

Leverage: None

Initial capital: $10,000

The window spans two major drawdowns and two recoveries, which gives the strategy plenty of real capitulation lows to fish.

The Results

The strategy won more often than it lost and still finished in the red, while simply holding Bitcoin over the same period returned many times more.

Why a 60% Win Rate Still Lost

This is the trap that makes bottom-fishing dangerous. The strategy was right six times out of ten. The problem was the size of the losses, not their frequency.

The winners were small bounces, exited early at RSI 55 by design. The losers were the times a capitulation low was not the low. Price kept falling, and those trades gave back far more than the small bounces earned.

A high win rate hides this. It counts how often you were right, not how much you made when right versus how much you lost when wrong. Here the average loss overwhelmed the average win.

The Real Cost: What You Gave Up

The most striking number is the comparison. Holding Bitcoin from 2020 to 2026 returned +714.1%. The bottom-fishing strategy lost 9.2% over the same period.

By selling every bounce at RSI 55, the strategy repeatedly cut its exposure right before the largest sustained recoveries. Bottom-fishing is built to capture small bounces, so it structurally misses the big trends that create most of Bitcoin's long-term returns.

The one genuine benefit shows up in drawdown. The strategy's worst drop was 40.4%, versus 76.6% for buy-and-hold. It was a smoother ride. It just did not go anywhere.

What Would Improve It

The backtest exposes the weaknesses, which is the point. Reasonable next tests you can run yourself:

Let winners run. Replace the fixed RSI 55 exit with a trailing stop, so the trades that turn into real recoveries are not cut short.

Add a trend filter. Only fish for bottoms when a longer-term signal suggests the broader trend is turning, to avoid buying into the middle of a crash.

Size the risk. Smaller positions on the deepest, riskiest entries can cut the size of the losers that did the damage.

Each change is a separate backtest. That is how you turn a losing idea into a tested one, or confirm it should stay on the shelf.

The Takeaway

Bottom-fishing Bitcoin looked reasonable and won most of its trades, yet lost money and trailed a passive hold by a wide margin from 2020 to 2026. The win rate was a comforting illusion. The losses, and the missed uptrends, were the real story.

If you are tempted to buy the next capitulation low, test your exact rules first. The data will tell you whether you are catching bounces or catching falling knives.

Why Bottom-Fishing Feels So Right

Bottom-fishing has powerful psychological pull. Buying when everyone else is scared feels contrarian and smart, and the story writes itself: get in at the low, ride the recovery, look like a genius. The problem is that the story is built on the trades that worked and quietly forgets the ones that did not.

Our backtest is a useful antidote. The strategy won 60% of its trades, which feels like success, and still lost 9.2% while buy-and-hold returned +714%. Being right most of the time is not the same as making money, and bottom-fishing is where that gap is widest.

The Two Problems That Sank It

First, the bottoms that kept falling. A rule that buys deep oversold readings will, in a real bear market, buy several times on the way down. Each of those looked like a bottom and was not. A few of those trades did most of the damage, which is why a 60% win rate still produced a loss.

Second, the trend it missed. By design, bottom-fishing exits on the bounce. That means it was out of the market for the sustained uptrends that produced almost all of Bitcoin's +714% over the period. Catching bounces is a fundamentally different game from capturing trends, and over six years the trends were where the money was.

The one genuine upside was risk. The strategy's 40.4% max drawdown was far gentler than buy-and-hold's 76.6%. Less pain, but also far less gain, and net negative once the deep losers were counted.

What Might Actually Improve It

A trend filter. Only fish for bottoms when a longer-term trend is up, to avoid catching every knife on the way down.

Let winners run. Replace the quick bounce exit with a trailing stop so recoveries that become trends are not cut short.

Smaller size on the deepest dips, to shrink the losers that did the most damage.

Each of these is a separate hypothesis, and each is a separate backtest. That is the honest way to turn a seductive idea into a tested one, or to retire it.

Frequently Asked Questions

Does buying the bottom ever work?

Sometimes, on individual trades. As a mechanical standalone strategy over this period it lost money and badly trailed holding. The feeling of success came from the winning trades, not the overall result.

Why did a 60% win rate still lose?

Because the losing trades were larger than the winning ones. Win rate ignores the size of wins and losses, which is why it can be misleading on its own.

Disclaimer:

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All strategies and examples are for illustrative purposes and do not guarantee results. Always conduct your own research before making financial decisions.

Key Takeaway